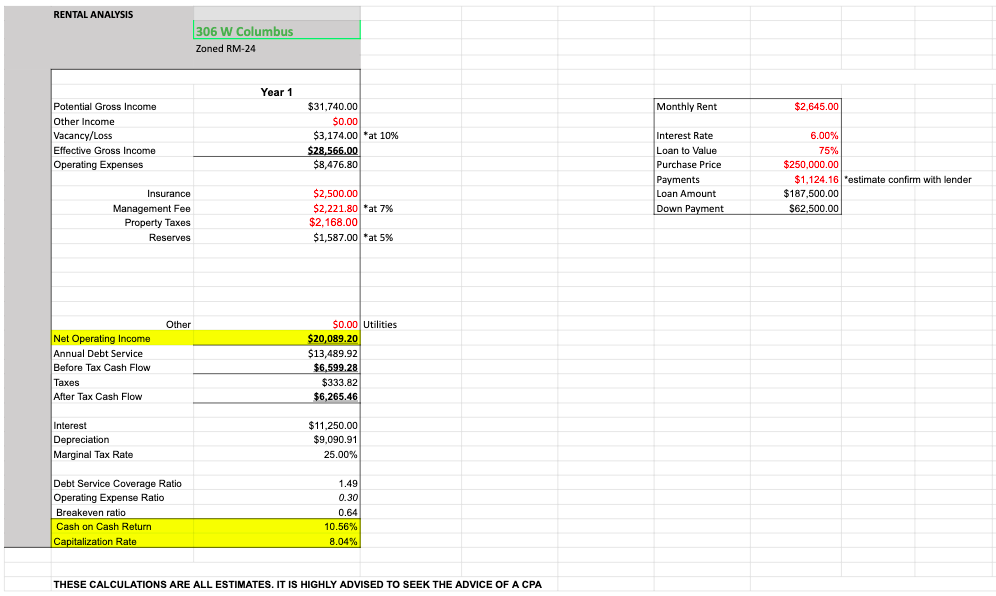

Are you a new investor or wanting to get started investing? You have probably seen cap rate this and cap rate that from every wholesaler, investment website, and realtor you have come in contact with, but what does it actually mean? Let’s start with some basic terms. For example purposes, let’s look at a property that has a monthly income of $2,645 and a purchase price of $250,000.

Potential Gross Income (PGI). The total rent that the property can generate at 100% occupancy.

ex) $2,645 x 12 mo = $31,740/yr

Vacancy & Loss. When you own income properties, there are going to be times that you will not be getting income such as: tenant turn over, late payments, non-payment, etc. This is just part of the game, so we try to account for it. For a quick evaluation, we use 5-10% of the PGI for vacancy & loss. If a property has a longer rental history, we can use this and general local information to narrow this number down.

ex) $31,740 x 0.10 = $3,174

Effective Gross Income (EGI). Potential Gross Income + Other Income – Vacancy & Loss. If a property has on site laundry or any other income, you add it here to get your effective gross income. (In our example, there is no additional income)

ex) $31,740 – $3,174 = $28,566

Operating Expenses. Any expense you incur to keep your operation running. Some of these include (but aren’t limited to): insurance, management fees, property taxes, reserves, HOA dues, and landlord paid utilities.

-For insurance, you can get a quick quote from an insurance broker or

ask the current owner what they pay.

-Management fees vary depending on the property manager and the

number of units you have the property manager handling for you. In

our example, I did 7% of the PGI because it was for a client that does

a lot of business with me. If you are running numbers on your own,

10% of the PGI is a fairly safe number.

-Previous year’s taxes can be found on the listing or on the county’s tax

collector site. You can also get an estimate for the current year’s taxes

online in most counties.

-Reserves are what you should put away for a rainy day (repairs,

attorney fees, etc). If the property needs a lot of work, you should use a

higher number. If the property is new construction, this can be a lower

number. I typically do 5% of the PGI for reserves for quick calculations.

For our example, the insurance is $2,500/yr, management fee is $2,221.80/yr, taxes are $2,168/yr, and the reserves are $1,587.

Net Operating Income (NOI). This is your actual income per year after all vacancy, loss, and operating expenses. Simply put, it’s EGI – Operating Expenses

ex) $28,566 – $8,476 = $20,089.20

Capitalization Rate. AKA Cap Rate is a ratio of the NOI to the Purchase Price expressed as a percentage. This is that term that you keep hearing about that is supposed to tell you the rate of return or the profitability of an income producing asset.

ex) ($20,089.20 / $250,000) x 100 = 8.04%

You now know exactly what the cap rate is and how it is calculated. Unless you are buying a property cash (which I never recommend), this number is irrelevant. So, what do I look at? I look at the Cash on Cash returns.

Cash on Cash. Cash on Cash is almost identical to the cap rate except it is a ratio of your before tax cash flow to your down payment.

Let’s break this down a little bit.

-Always leverage your money. If you have $250,000 cash, you can buy

one $250,000 property cash OR you can leverage your money (finance

the properties) and get TEN $100,000 properties.

-Your downpayment is typically going to be 20-25% down unless you are

using a specialty program.

–Before Tax Cash Flow is your NOI – annual debt service

–Annual Debt Service is your (Principal + Interest) x 12

ex) In this example, we will do 25% down and a 6% interest rate.

($6,599.28 / $62,500) x 100 = 10.56% Cash on Cash Return

Here’s an example of what I send to my clients for an initial analysis of a property.

So what makes for a good return? It depends on what you are looking for and what your investment strategy is. Don’t have a strategy? We can help with that.

Maybe you’re already experienced and have a set strategy, but you want somebody else to do the due diligence for you, we can do that as well.